After the Reserve Bank of India’s announcement that pricing of floating interest rate loans should have its repo rate as the external benchmark from 1 October 2019, people have been wondering about how this will impact their home loan EMIs. Whether you already have a home loan going on for a number of years or are thinking of applying for one now, this is something that will definitely have an impact on you. It is important to understand how linking of interest rates on home loans to repo rates of the Reserve Bank of India will impact you because now your credit score too plays an important factor in this equation.

What is the repo rate?

To put it simply, the repo rate is the rate at which banks borrow money from the Reserve Bank of India. When loan interest rates were not linked to the repo rate, but to the Marginal Cost of Funds Based Lending Rate (MCLR) as the external bench mark, any cuts in the repo rate were not passed onto the customer by the banks, but the recent fluctuation in repo rates has resulted changes in the home loan interest rate all banks 2019.

Repo-Rate Linked Lending Rate (RRLR) will help to bridge this gap and ensure that, with the Reserve Bank of India announcing numerous cuts in the basis points (bps) this year, all these cuts are also passed onto the customer.

A repo rate cut of 35 bps, for example, will bring down an interest rate that was 8.4% to 8.05%. Again, even though there is a reduction, how much it will be individually would depend on the loan slabs and the risk profiles of the loan borrowers.

The link to your credit score

The link of the new system to your credit score stems from the fact that the RBI has also allowed banks to charge a credit-risk premium over the external benchmarks when it comes to calculating the effective interest rate for each individual home loan borrower. This is what makes the credit score of borrowers an important aspect of the new loan interest rates.

What is risk-based pricing?

In risk-based pricing, the rate of credit is dependent on the credit score of the borrower. So borrowers are typically categorised according to their credit scores which will segregate them into different risk profiles. This is good news for those with good and high credit scores as they can expect banks to woo them with a whole host of favorable terms and conditions, such as lower interest rates compared to others with a lower credit score.

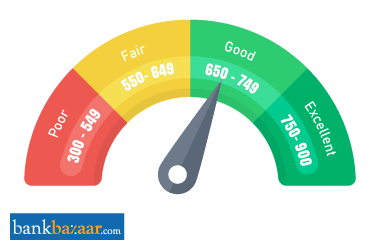

The past credit history of the applicant can be obtained through credit rating agencies that are approved by the Reserve Bank of India, such as CIBIL. Those with good credit ratings or scores are deemed as low risk for defaulting. This is because a good credit score is built up over time by paying off your dues on credit cards and loans without any delays or defaults. These are the kind of borrowers that banks want and so they will woo such borrowers with lower interest rates.

Banks are offering different interest rates to different categories of risk profiles. For example, a leading bank offers three different interest rate variations on their home loans based on three different CIBIL credit score slabs. The upper limit being 900, those with a score of above 760 are offered an interest rate of 8.1%. Those with a score between 675 to 724 are offered 9.1% while those between 729 and 759 have to pay 8.35%.

This is a huge difference when it comes to the EMIs and can be a huge difference when it comes to savings.

Get your credit score right

|

| Image Credit: BankBazaar.com |

A credit score above 760 is considered to be high whereas anything less than that is considered to be low and therefore high risk. Such high-risk applicants will be offered higher interest rates on their retail loans, whether it is a home loan, personal loan, or vehicle loan.

It is not enough to just have a good credit score at the time of applying for the loan. This should ideally be maintained throughout the tenure of the home loan as well.

Some banks will even change interest rates if you delay payments on the home loan more than 3 times in a year (for more than 30 days each time). It is also wise to stay away from multiple credit cards and loans as these can also bring down your credit score if you are not able to pay back the outstanding dues on time.

The flip side is that if your credit score increases, the bank could also reduce your interest rate. Even a one-point reduction will result in thousands of rupees saved, which is something to work towards.

Comments

Post a Comment